Second-Hand Software: From Cost Center to Financial Lever

Most organizations treat software as a necessary expense.

It is budgeted, negotiated, and managed—but rarely questioned at a structural level. The assumption is simple: software is something you buy, use, and eventually replace.

That assumption no longer holds.

Across industries, software spend is becoming less predictable, less flexible, and increasingly disconnected from actual usage. At the same time, significant value remains locked within existing license portfolios—unseen, unmeasured, and unutilized.

The result is not just inefficiency.

It is a missed financial opportunity

The Visibility Gap

Over the past few years, the dynamics of software licensing have shifted materially. Vendors have moved toward subscription-based models, tightened contractual frameworks, and reduced flexibility in how licenses can be deployed.

The changes following VMware’s acquisition by Broadcom are a clear example. Many organizations are now facing increased costs alongside reduced control over their licensing strategy.

Yet while external pressure has increased, internal visibility has not kept pace.

In many organizations, it remains difficult to answer fundamental questions with confidence:

Which licenses are actively used?

Which are redundant?

Which still hold recoverable value?

Without that visibility, software continues to be treated as a static cost—despite behaving more like a dynamic asset.

An Untapped Asset Class

When physical infrastructure is decommissioned, companies increasingly expect financial return. Hardware is assessed, valued, and monetized as part of standard lifecycle management.

Software, by contrast, is often written off.

Licenses that are no longer required—whether due to cloud migration, consolidation, or changing operational needs—remain on the balance sheet without being actively managed.

This is not a technical limitation. It is a mindset gap.

Within the EU, the resale of perpetual software licenses is legally established, provided that usage is discontinued and the transfer is properly documented. In other words, these licenses can move—just like other assets.

The implication is straightforward:

software is not only a cost. In many cases, it is also a source of recoverable value.

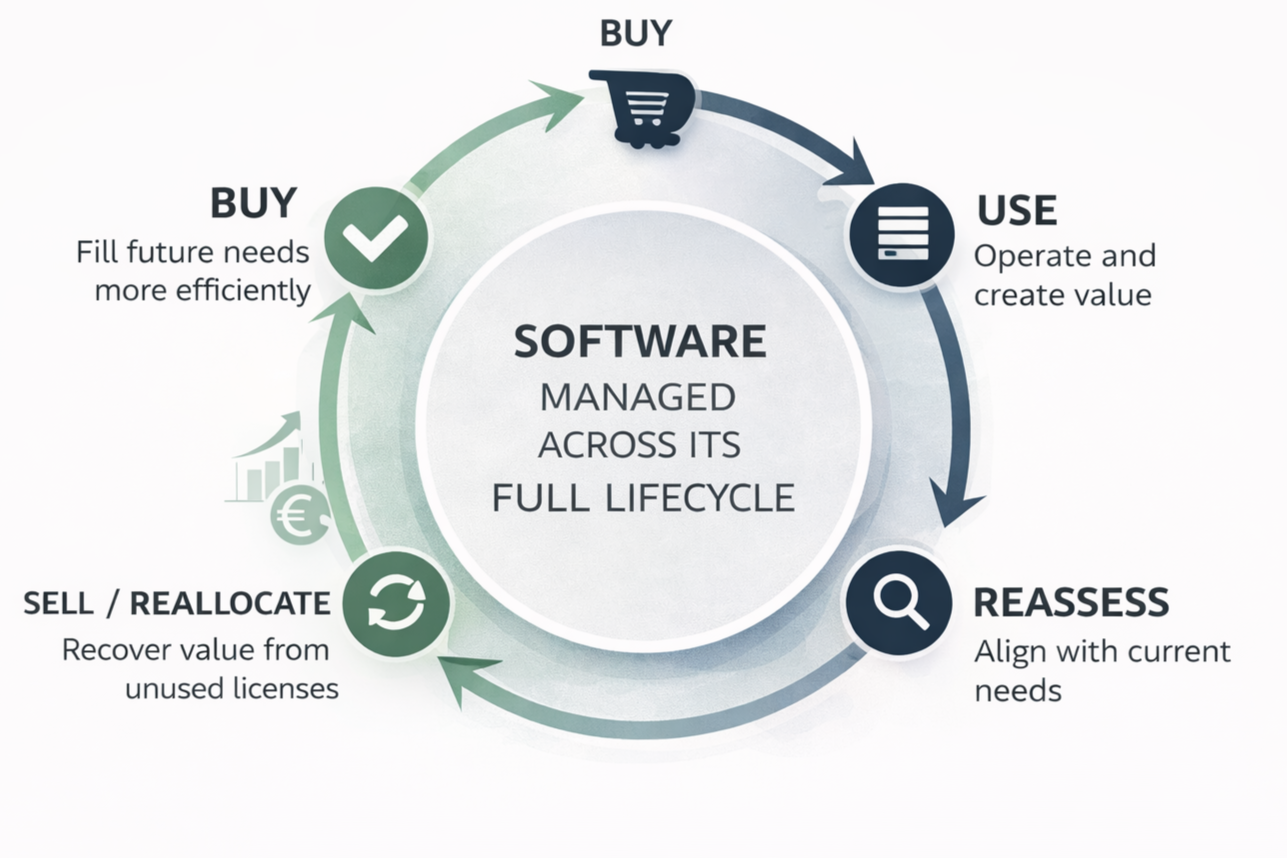

Reframing the Decision: Buy vs. Recover

The conversation around software typically begins at the point of purchase.

What needs to be acquired? At what price? Under which terms?

A more strategic starting point is to consider the full lifecycle.

Before acquiring new licenses, organizations should ask:

What do we already own?

What is still required?

What can be redeployed—or recovered?

This shift changes the role of software within the organization. Instead of a linear cost, it becomes a lever that can be adjusted in multiple directions.

On one side, unused licenses can be divested, unlocking capital that would otherwise remain dormant. On the other, new requirements can be fulfilled more efficiently through the secondary market, reducing overall spend without compromising operational needs.

Individually, these actions create incremental improvements.

Combined, they introduce structural flexibility into the IT cost base.

Where This Approach Creates Value

This model is not universally applicable, nor should it be.

It is most effective in environments characterized by stability rather than constant change—where infrastructure is mature, and where the value of continuity outweighs the need for continuous upgrades.

In these contexts, the assumption that “new is necessary” often deserves scrutiny.

Conversely, in highly dynamic or cloud-native environments, vendor alignment and access to ongoing innovation may remain the priority. The objective is not to replace existing strategies, but to complement them where it makes sense.

The distinction is important.

This is not about cost-cutting. It is about capital efficiency.

Execution Risk Is Not Where Most Assume

Skepticism around second-hand software typically centers on compliance and risk.

In practice, the risk rarely lies in the concept itself, but in its execution.

Poor documentation, unclear ownership history, and weak internal controls can create exposure—particularly in audit scenarios. Conversely, a structured approach with full traceability and clear contractual frameworks mitigates these concerns effectively.

In that sense, software should be treated no differently than other regulated assets. The discipline applied to financial reporting is equally relevant here.

From Operational Topic to Financial Discipline

Perhaps the most significant shift is not operational, but organizational.

Software decisions often sit between IT, procurement, finance, and compliance. As a result, no single function owns the full picture.

Elevating software from an operational concern to a financial discipline requires alignment across these functions. It requires a shared understanding that software is not simply consumed—it is managed across its lifecycle.

Organizations that succeed in this shift do not necessarily spend less.

They spend more deliberately.

A Different Starting Point

The most effective way to begin is not with the market, but internally.

Not by asking what to buy—but by understanding what already exists.

From there, the options become clearer:

what to retain

what to redeploy

what to divest

and what to acquire differently

This is not a complex transformation. But it does require a change in perspective.

Closing Perspective

For years, software has been treated as a fixed cost within IT budgets.

That perception is increasingly out of step with reality.

As licensing models evolve and financial pressure increases, the organizations that adapt will be those that treat software not as a static expense, but as a dynamic lever—capable of being optimized, reallocated, and, where appropriate, monetized.

The question is no longer only what software costs.

It is what it is worth.